Nathan Latka at SaaSiest 2026: 9 case studies, 3 patterns

By Mohammed Alsaadi

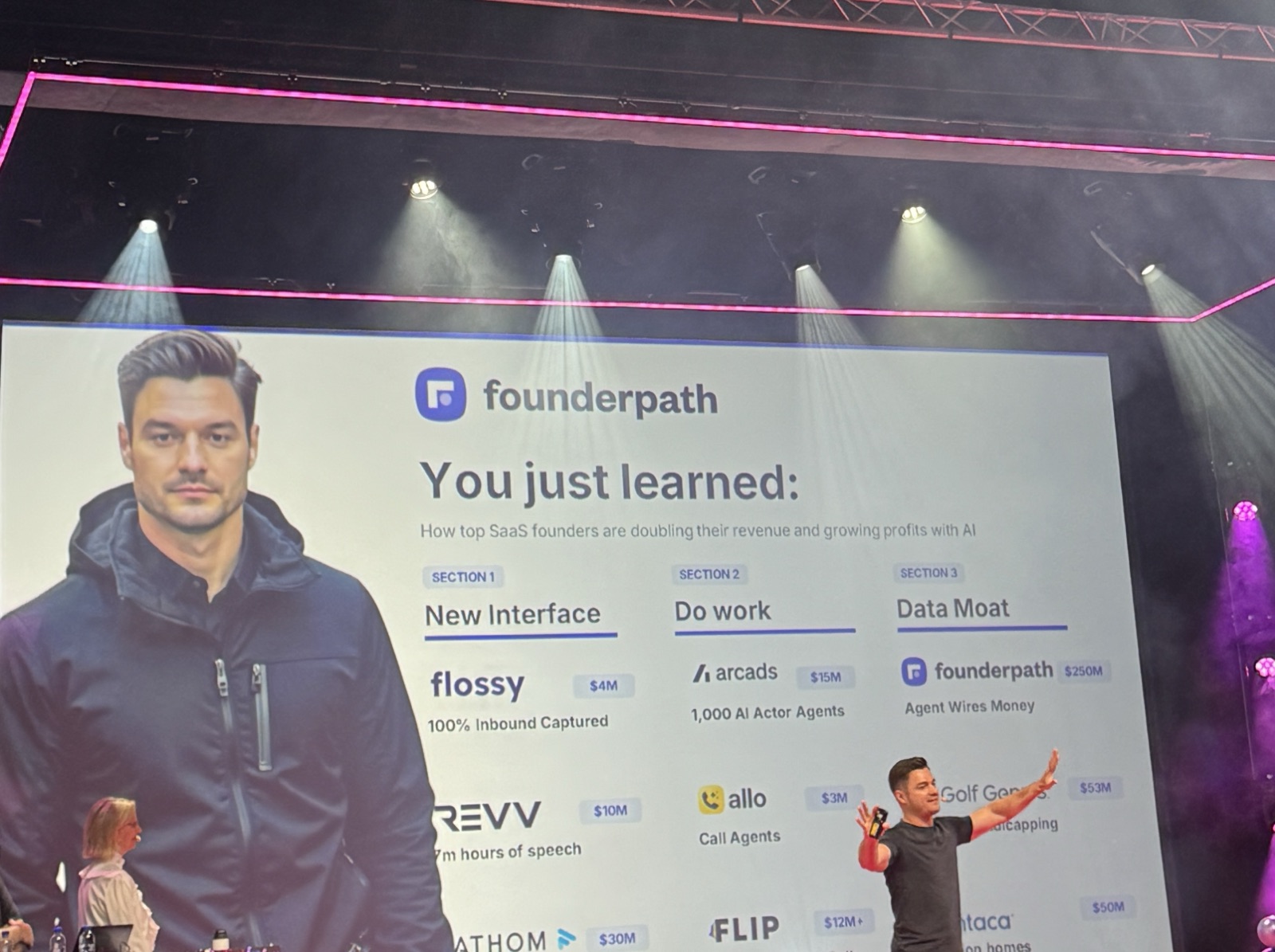

SaaSiest 2026 just wrapped in Malmö. Nathan Latka, CEO of Founderpath, opened with one of the more useful talks of the event. Nine real case studies of private software companies that are growing right now, in the age of AI, and the patterns that actually explain it.

His framing: the public markets are punishing software companies, headlines say SaaS is dying, and yet there are private companies going from $1M to $30M ARR in 18 months. Why? Three patterns repeat across all nine.

Pattern 1: Price against jobs to be done, not seats

Three companies, three flavors of the same pivot.

Flossie. Dental practice software. In 2022, they sold scheduling tools to dentists. By 2026, they sell Fiona and Betsy: AI agents that book patients, re-engage no-shows, and chase recall appointments. Same problem space, different unit of value. They went from $1M to $4M ARR fairly fast. The pricing move that mattered: charging per location, not per seat. Latka's framing:

"It's not even usage-based pricing. You actually want the most usage so you can go to your data moat."

The other piece: setup fees. They used to be considered amateur. Pure SaaS, no professional services revenue. The new wisdom: setup fees buy you the data integration work that becomes your moat.

Vantica + HOAi. Homeowners-association software. Acqui-hired HOAi (YC) in late 2024. HOAi is "an agent that lives inside Vantica relentlessly pursuing all the tasks humans would have used Vantica to do." Billings, invoice payments, customer questions about bills. Per-door pricing across 6M homes. Recently valued at $1.3B with $300M secondary done.

Allo. Result-as-a-service. From their founder:

"Most SaaS today is a dashboard you pay your employee to move information around. With Allo, the employee can still use the dashboard, but AI agents are doing actions on their behalf."

Pattern across all three: stop pricing for software access. Price for the work getting done. Per location, per door, per result. The unit of value scales as the customer scales.

Pattern 2: Data + integrations are the moat now

If you control your customer's brain, you control their next AI vendor decision.

Rev. Auto-repair shop software. $1M ARR in 2023, $4M in 2024. The play: integrations. When a car comes into the shop, Rev runs in the background, does the research the technician would have done, and surfaces components and parts at the technician's fingertips. None of it works without deep integrations into shop systems. Latka turned this into a direct call-out for the room:

"If your competitors will build trust faster and offer more integrations, go to your integrations page and count. If you're less than your competitor, that's a very strong signal your competitor is in a better position to win in the age of AI."

Fathom. AI notetaker, $30M ARR, raised very little. Founder Richard White bet six years ago on AI cost coming down before the curve was visible. Cost per minute of transcription dropped from $3.50 to under a penny. He told Latka:

"We bet on that, and we bet on Gen AI getting really good. We said, hey look, it's not here yet, but we think it's going to get really good."

The point: inference cost is going to keep dropping. What work could you do for your customers if it cost you 10% of what it costs today?

Founderpath. Latka's own company. $250M deployed across roughly 700 software companies with a team of five. The mechanism: they connected their chat interface to the fund's bank account. A founder applies for capital, the chat writes the underwriting memo on the back end, approve or reject decision instant.

"If you trust me with your data, you trust me with your brain, I give you capital faster."

Founderpath has 4,500 Stripe accounts connected. Their question now: what other work can they do with that brain? That's the move. Turn data trust into adjacent revenue.

Pattern 3: Closed-loop systems beat chat boxes

Most SaaS dashboards now have a chat box on the right. Most are bad. The next thing is closed-loop systems where the user states an outcome and the agent runs the whole job without being prompted again.

Arc Ads. AI-actor video ads at scale, sells to CPG brands. Bootstrapped, around $15M ARR with 8 people. That's roughly $1.9M revenue per employee. Latka's benchmark: the new bar for revenue-per-employee is $400-600K, up from the old $200K.

The closed-loop move: instead of a chat where someone types and reads a response, the user types something like:

"Spend $5,000 testing a thousand ad variations optimized for 2x ROAS in 30 days."

Then the agents run in the background, hit the target or don't, and the system kills what didn't work. That's a closed loop. The dashboard interface stays. The work moves to agents.

Golf Genius. $50M+ ARR. The official handicapping app. 8M users. Latka's point here was different: AI is not killing SaaS, it's making more competition possible. The moat isn't the software anymore. It's the regulatory positioning, the SOC 2 / PCI compliance, the payment rails. "It's going to be hard for agents to become PCI compliant. Think about that."

Latka pushed every founder in the room to think of one or two closed-loop experiments to launch inside their own dashboards this quarter.

Why this matters

Latka's three patterns map cleanly onto a thesis Opmore already runs on:

- Pricing against jobs to be done is the operator version of "the value is in the work, not the access." It's also why founder-led services compress on multiple. The work isn't separable from the person doing it.

- Data and integrations as the moat is the SaaS version of context. The deeper your customer's data is connected to you, the harder it is to rip you out, regardless of what the AI underneath looks like next year. That's the wedge for the SMB founders we work with: the context layer for companies that haven't documented anything yet. Data trust precedes capability.

- Closed-loop systems beat chat boxes is the operator version of agents on top of context. Chat is the entry point. The moat is what the agent can finish without you in the room.

The companies Latka picked aren't outliers. They're what's working at $1M-$30M ARR right now. Founders running smaller companies don't need a different playbook. The same patterns apply, the units are smaller.

Three honest answers to three questions and you have your roadmap for the quarter:

- What can you charge against (a job to be done) instead of seats?

- What integrations do you need to launch to become the brain for your niche?

- What's one closed-loop experiment you can ship inside your dashboard this month?

Join the newsletter.

A weekly summary of new insights, plus what's new at Opmore. No spam, just insights.